Markets Rewarding Discipline

Jake DeKinder, Head of Advisor Communication at Dimensional Fund Advisors Ltd, explains how capital markets have rewarded investors that are able to tune out short-term noise and stay disciplined over the long-term.

![]()

Jake DeKinder, Head of Advisor Communication at Dimensional Fund Advisors Ltd, explains how capital markets have rewarded investors that are able to tune out short-term noise and stay disciplined over the long-term.

The popular National Savings & Investments (NS&I) savings certificates will be indexed to CPI instead of RPI from next year.

The certificates have not been on sale since 2011, but NS&I allow existing certificate holders to reinvest in new series of certificates when their old ones mature. The terms have gradually worsened over the years and at present reinvestment promises a return of RPI inflation +0.01% a year. For certificates maturing from 1 May 2019, the basis of indexation will change from RPI to CPI.

The change was not picked up by newspapers at the time because they were released the Friday before the 2018 Budget, held on the Monday. Government departments are often accused of burying bad news, and the downgrading of the NS&I index-linked savings certificates is certainly bad news for affected investors.

The government now generally only uses RPI where it benefits, for example as the basis for interest levied on student loans or for annual rail fare increases. CPI is used to index many – but not all – income tax bands and allowances.

NS&I said, ‘This change recognises the reduced use of RPI by successive governments and is in line with NS&I’s need to balance the interests of its savers, the cost to the taxpayer, and the stability of the broader financial services sector.’

As the graph shows, the move from RPI to CPI will cut returns by about 0.8% a year based on data since 2010. In their widely-missed press release, NS&I note that, ‘The cost to the taxpayer is forecast to reduce by £610 million over the next five years’. That ‘cost to the taxpayer’ could also be read as, ‘return to the investors’.

If you hold any issues of index-linked certificates, think about whether you definitely want to reinvest when they next mature, rather than letting inertia (and automatic reinvestment) take its course.

The value of investments and the income they produce can fall as well as rise. You may get back less than you invested.

The State Pension Age (SPA) became equal for men and women for the first time, at age 65, on 6 November 2018.

Having reached this landmark, the next stage of SPA increases has already started. For both men and women, the state pension will become payable for anyone born between 6 December 1953 and 5 January 1954 on 6 March 2019. The SPA will then be increased to reach age 66 by October 2020.

The SPA is scheduled to rise again as existing legislation already covers the increase from 66 to 67, phased in over two years from April 2026. The same legislation provides for a step up to 68, starting in April 2044.

However, in July 2017 the Department for Work and Pensions announced it would accept the recommendations of the Cridland Review – this brings the start of the move to a SPA of 68 forward to April 2037. Legislation for this change has been deferred until after the next SPA review in 2023 – raising the SPA in the current political conditions could prove difficult for the government – but if your SPA will be at least 68 if you were born after 5 April 1971.

The rising SPA is linked to historic improvements in mortality – in effect they match the increases in life expectancy at age 65 of 8 years for men and 9 years for women since the early 1950s.

The Cridland Review has anticipated future increases in life expectancy as an argument for accelerating the increase in SPA. However, data from the Office for National Statistics issued in September, suggest that increases in life expectancy may have come to an end, at least for the time being.

The arrival of the equalised SPA provoked a fresh round of protests from women born in the 1950s, who started working life with an expectation that their state pension would be payable from age 60. The government has previously made a minor concession on the phasing of the change but further offers are not expected. The simple reason is cost: a higher SPA reduces government pension expenditure and raises extra National Insurance Contribution revenue.

If you want to retire when you choose, rather than the State decides, make sure your private pension provision is adequate.

The value of your investment can go down as well as up and you may not get back the full amount you invested.

Past performance is not a reliable indicator of future performance.

The government has revived plans to raise probate fees in England and Wales.

A new, banded structure for probate fees in England and Wales is to be introduced, according to a written statement issued a week after the 2018 Budget by the Parliamentary Under Secretary of State for Justice.

The announcement comes after the absence of inheritance tax (IHT) reforms in the Budget, despite the Chancellor commissioning a review by the Office of Tax Simplification in January 2018. The only change to IHT announced in October was a small adjustment to the legislation for the residence nil rate band – this being such a complex piece of legislation, it had been wrongly drafted.

If new probate fees sound familiar, it is because a very similar announcement was made in March 2017. At the time the proposal provoked widespread criticism, because the higher levels were seen to be more of a new tax than a simple fee adjustment. In the event the planned change fell victim to the legislative logjam around the last General Election and disappeared.

Since then, the government has taken on board some of the original criticism and cut the fees they are proposing, particularly for larger estates.

The current fees are £215 for individual applications and £155 via a solicitor, with nothing payable if the estate value is up to £5,000. Under the new banding, there is a maximum effective charge for probate of 0.5% of the estate, which is triggered at £50,000 (a £250 fee) and £500,000 (a £2,500 fee).

The new fees are currently scheduled to come into effect 21 days after the legislation is passed, and there is very little that can be done to mitigate the impact. They are payable even if the estate passes with no IHT liability, as is usually the case on the first death of a married couple or civil partners, or if the value of the estate is covered by the available nil rate and residence nil rate bands.

There are still opportunities to save IHT with careful planning and, as the Budget made no significant changes, there remains a window of opportunity before any reforms are introduced.

If you would like help updating your estate plans ahead of the review publication please get in touch.

| Value of estate | Old Proposal |

New Legislation |

| Up to £50,000 or exempt from requiring a grant of probate | Nil | Nil |

| £50,001 – £300,000 | £300 | £250 |

| £300,001 – £500,000 | £1,000 | £750 |

| £500,001 – £1,000,000 | £4,000 | £2,500 |

| £1,000,000 – £1,600,000 | £8,000 | £4,000 |

| £1,600,001 – £2,000,000 | £12,000 | £5,000 |

| Over £2,000,000 | £20,000 | £6,000 |

The value of tax reliefs depends on your individual circumstances.

Tax laws can change.

The Financial Conduct Authority does not regulate tax or trust advice.

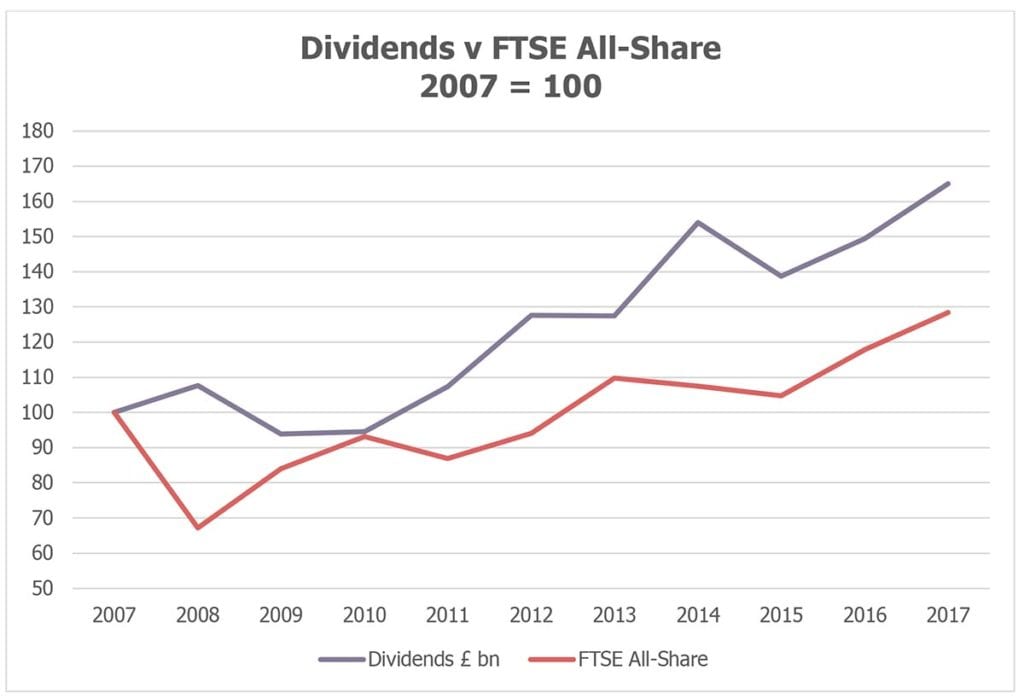

UK dividends are continuing to grow faster than inflation, according to the latest quarterly data from Link Asset Service.

The latest UK Dividend Monitor (UKDM) shows that in the third quarter of 2018 dividend payments were 4.1% up on the previous year, comfortably above the current rate of inflation. Looking over the 10-year period from the end of 2007 to the end of 2017, total dividend payments have risen by an average of 5.1% while CPI inflation has averaged 2.4%.

The UKDM is published by Link Asset Services (formerly produced by Capita) and totals the dividends paid out on the ordinary shares of companies listed on the UK Main Market every quarter – excluding investment companies, to avoid double counting. It captures both regular dividends and one-off special dividends, which often stem from takeovers or other corporate restructurings.

As the graph shows, over the last ten years, the amount paid out in dividends has grown faster than the capital value of shares. There are still dips, but between 2007 and 2017 the regular dividend total dropped only once, in the wake of the global financial crisis. The jump and dive between 2013 and 2015 is an aberration caused by a one-off £15.9 billion special dividend paid by Vodafone in 2014.

Despite increasing dividend payments, there has been considerable volatility in UK share prices throughout 2018. Little more than five months, and over 1,000 points, separate the FTSE 100’s high and low marks for the year to date. But whilst the FTSE tracks capital values, it does not account for dividends, which are ignored in the calculations of most equity market indices.

If you are investing for income the data is a reminder that, for all the fluctuations in capital values, shares have continued to provide real dividend growth.

The value of your investment can go down as well as up and you may not get back the full amount you invested.

Past performance is not a reliable indicator of future performance.

Investing in shares should be regarded as a long-term investment and should fit in with your overall attitude to risk and financial circumstances.

The Office of Tax Simplification (OTS) has published the first part of its inheritance tax (IHT) simplification review.

The report highlights a variety of issues with the current IHT system:

The OTS made a key administrative recommendation: ‘The government should implement a fully integrated digital system for Inheritance Tax, ideally including the ability to complete and submit a probate application’. HMRC have already started such a project in 2014, and in April 2018 announced it would be delayed, choosing instead to focus on the short IHT205 form which applies to certain estates where no IHT is payable.

The Chancellor asked the OTS to undertake its review of IHT in January 2018. The instruction was, ‘to identify opportunities and develop recommendations for simplifying IHT from both a tax technical and an administrative standpoint’.

The OTS originally indicated it would publish a report ahead of the Autumn Budget, but Mr Hammond brought the Autumn Budget forward to October and nothing emerged from the OTS in time.

In late November, about the time the Budget would normally have arrived, the OTS published the first half of its review. Such was the response to the OTS consultation document, the organisation has decided to produce two reports. The first covers ‘administrative issues’ while the second will explore ‘key technical and design issues’.

The second report is due in spring, and could herald changes to tax rules, instead of the administrative framework. The result may be less generous than the current system, meaning it could be wise to review your estate planning opportunities now.

The value of tax reliefs depends on your individual circumstances.

Tax laws can change.

The Financial Conduct Authority does not regulate tax or trust advice.

Over the last few years, a number of regulatory changes have been introduced that have affected the profit that can be made from renting out buy-to-let properties. In addition, landlords are facing new regulatory demands.

Buy-to-let landlords will have their income tax relief on mortgage interest restricted to 20% by 2020, and that’s on top of higher Stamp Duty (and equivalent taxes in Scotland and Wales) and the recent rise in interest rates.

Buy-to-let mortgage advances fell by more than 10% in 2017, as the new tax rules came into effect. Over the period, the value of loans was down 12.3%, with the number of mortgages granted for this type of property falling by 10.4%. Many landlords are said to be considering their options; some are thinking of selling up, and others are remortgaging rather than taking out loans for new property purchases.

Some intent on staying in the market, are considering running their properties through a company, as the tax treatment is more favourable; 18% of private rentals in England are now owned by limited companies.

Over 70 local authorities have already introduced licensing for private landlords, with more considering this option. To be licensed, landlords need to meet tenant safety regulations and, in some cases, sign up to a charter. All private landlords in Scotland are required to register with their local authority and be on the Scottish Landlord Register. In Wales they must register with Rent Smart Wales.

The new criteria for Houses in Multiple Occupation (HMOs) will mean that 177,000 properties will need to be licensed. Property occupied by five or more people from two or more households will be considered an HMO, and must meet fire, gas and safety requirements.

In 2019, the proposed ban on residential letting fees for tenants is expected to come into force (Scotland introduced a ban in 2012). This means that common charges associated with reference checking or application processing will be outlawed, and agents may pass these costs on to landlords. The government also plans to introduce compulsory three-year contracts for residential lets in England.

Despite the changes, it is still possible to make a success of buy-to-let. It pays to do your homework and consider the balance between rental yields and capital growth. Location is as important as ever, so too is knowing your market and positioning your property accordingly.

Your email account can be a treasure trove for cyber criminals. New research has revealed that 79% of people keep emails in their account that can be exploited by cyber criminals to commit Identity theft, fraud, or impersonation.

Cyber Aware is warning the public that without using a strong and separate password for your main email account, you risk giving cybercriminals a wealth of information that could be used against you.

This comes after research from UK General Insurance in partnership with Cyber Aware reveals that people are storing sensitive information within their email accounts. 51% of people store e-receipts revealing purchase history, 34% store personal photos of friends, family or pets and 6% have love letters saved in their inbox.

Storing this kind of information can be like ‘gold dust’ to criminals, who can use it to commit cyber crime including making phishing emails more convincing by including personal information or impersonating you or friends and family.

National Cybercrime Programme Lead, Detective Superintendent Andrew Gould from the National Police Chiefs’ Council said: “Just imagine someone posing as you and the reputational, emotional and financial damage it could do to you and your loved ones. The Cyber Aware campaign wants to make people really think about the value of our inboxes and treat them in the same way we treat treasured possessions in the offline world.”

Alison Marriott, a victim of hacking said: “The whole experience was very distressing. emails were being sent from my account to my contacts which I had no control over. It caused a great deal of embarrassment as there were lots of phone calls to be made to explain the situation. It was also very inconvenient and took days to sort out.”

Cyber Aware has released the following tips as part of its #OneReset awareness campaign:

If you have been affected by this, or any other scam, report it to Action Fraud by calling

0300 123 2040, or by using the online reporting tool at www.actionfraud.police.uk

By clicking on one of these links you are departing from the regulatory site of Polestar. Neither Polestar nor Positive Solutions is responsible for the accuracy of the information contained within the linked site.

Research carried out by the Pension & Lifetime Savings Association shows that the majority of people would find it much easier to plan for retirement if they had income targets to guide them.

The trade body is proposing three target levels covering ‘minimum’, ‘modest’ and ‘comfortable’ incomes and recommends carefully-chosen titles to ensure they are correctly interpreted. This approach is already used in Australia where it is said to make it much easier for savers to work out if they are saving enough.

According to a recent report entitled “Will we ever summit the pensions mountain?”1 the amount that the average person will need to fund a comfortable retirement, based on someone opting to stop work at 65 and buying a singlelife annuity with inflation protection, has reached £260,000.

The report also points out that those who don’t make it onto the housing ladder will need to pay rent during their retirement years, so for them the figure will be even higher at £445,000. In arriving at these figures, the research assumed average earnings of £27,000 a year, and a full state pension of just over £8,500.

The sooner you start, the longer your contribution has to grow.

One of the most attractive features of pension saving is the tax relief. If you make contributions to a pension, or if your employer deducts your payments from your salary, you automatically get 20% tax relief as an additional deposit into your pension pot. If you are a higher-rate taxpayer you can claim an extra 20%, while those paying additional-rate tax can claim back an extra 25%. When you retire, you can take 25% of your savings as a tax-free lump sum, though not necessarily all in one go. If you save into a workplace pension, your employer should match some or all of your contributions, providing a welcome boost to your pension.

Everyone would like to look forward to a financially-comfortable retirement that can be enjoyed rather than endured. Taking financial advice will ensure that you put the right pension plans in place from the outset and know what your savings target should be. You’ll also be offered regular reviews to help ensure you keep your pension savings on track.

If you’re making plans for your retirement and would like some professional advice, then please get in touch.

1 Royal London, 2018

The value of pensions and the income they produce can fall as well as rise.

You may get back less than you invested.

The 2018 Budget – delivered on a Monday for the first time since 1962 – produced a number of surprises, not least some high-profile ‘giveaways’.

Announcements in the Budget included:

However, Mr Hammond’s generosity was not all it appeared. For instance, the personal allowance and higher rate threshold will both be frozen in 2020/21, while the business rates reduction and higher AIA will only last for two years. The Chancellor also kept many tax thresholds and allowances unchanged.

A good example of the impact of frozen thresholds is the personal allowance that will continue to be tapered from an income level of £100,000. This threshold has applied since April 2010, and it creates high marginal rates for some taxpayers. Combined with the increase in the personal allowance, for income between the taper threshold of £100,000 and the starting point for additional rate tax of £150,000:

By far the largest element of spending announced in the Budget was for the NHS. Investment is £7.35bn out of a total £15.09bn in 2019/20, rising to £27.61bn out of a total £30.56bn in 2023/24. With such large amounts to secure for the health service, the Chancellor has limited scope to reduce personal tax in the medium term.

If you would like to discuss the impact of the Budget on your finances, please get in touch.

Tax laws are subject to change.

The Financial Conduct Authority does not regulate tax advice.