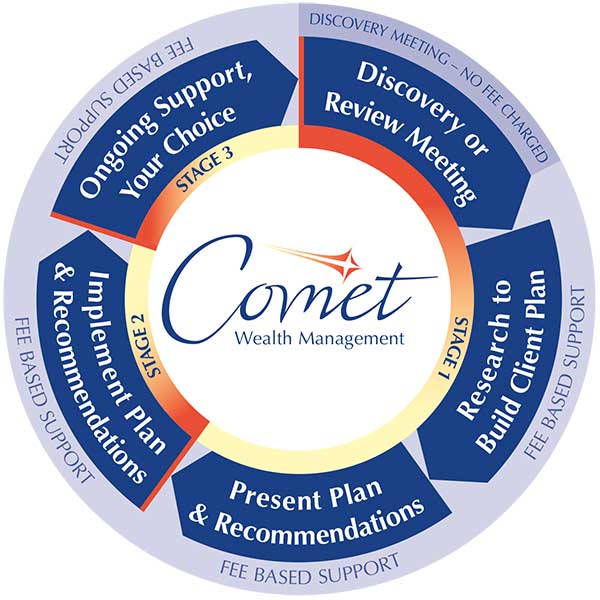

Stage 1.1) Discovery or Review Meeting

Your financial planner will start by listening carefully to your objectives, needs and priorities, in the context of your short, medium and long term financial aspirations.

By gathering information from you, they begin to understand your current situation and what provisions you have in place already.

Then, by exploring your hopes and aspirations, they can construct a picture of what you want to achieve, taking into account your knowledge, experience and attitude to risk and return.

This stage also allows you to understand what to expect from us and how you will benefit from using our services and is a neutral contribution of our joint time. This stage is NOT fee based.

Stage 1.2) Research to Build Client Plan

We’ll explore and research various scenarios and options and start to put together a road map to help you move towards achieving your objectives.

We will assess the suitability of your current plans and make recommendations to help you achieve your current and future objectives. This stage is fee based.

Stage 1.3) Present Plan & Recommendations

Your financial planner will sit down with you and go through your plan and recommendations answering any questions you may have. This stage is fee based.

Stage 2) Implement Plan & Recommendations

Here’s where your plans start to take shape. Most of our clients prefer us to complete, check and manage the documentation required for them to put ‘Their Plan’ into action. This saves them a lot of time and energy, and helps ensure that plans are set up in line with expectations. The cost of this service will be included in the fee structure that has been agreed.

Alternatively you may decide you wish to implement our recommendations yourself, and so can simply pay a fee for our time and expertise up to this point.

Should you choose to implement your plan and your choice of recommendations, your fee in 1.2 and 1.3 may be discounted against your stage 2 implementation fee.

Stage 3) Ongoing Support for You and Your Family

We believe that most clients will benefit from a review of their circumstances. This may depend on which stage of life you are in as well as your relative level of wealth.

Many clients like to meet up regularly to take advantage of valuable allowances, or understand the impact of UK Government Budget announcements.

You will also hear from us at other times during the year when we feel something may be of interest to you, or you may wish to get in touch yourself, if your circumstances or objectives have changed. This stage is supported by your ongoing fees.